Chancery Lane chief executive officer Doug Brodie has challenged claims actively managed funds cannot beat the market.

He told Money Marketing research and reports “invariably” comment on investing in US equities, where managers have traditionally struggled to beat the S&P500.

“Struggled, not failed altogether as we remember Bill Miller’s educational trumping of the index for 15 consecutive years whilst at Legg Mason,” Brodie said.

Active investment has been put into question recently.

But Brodie said that the performance of the investment style differs depending on the methodology, for instance with the inclusion of investment trusts.

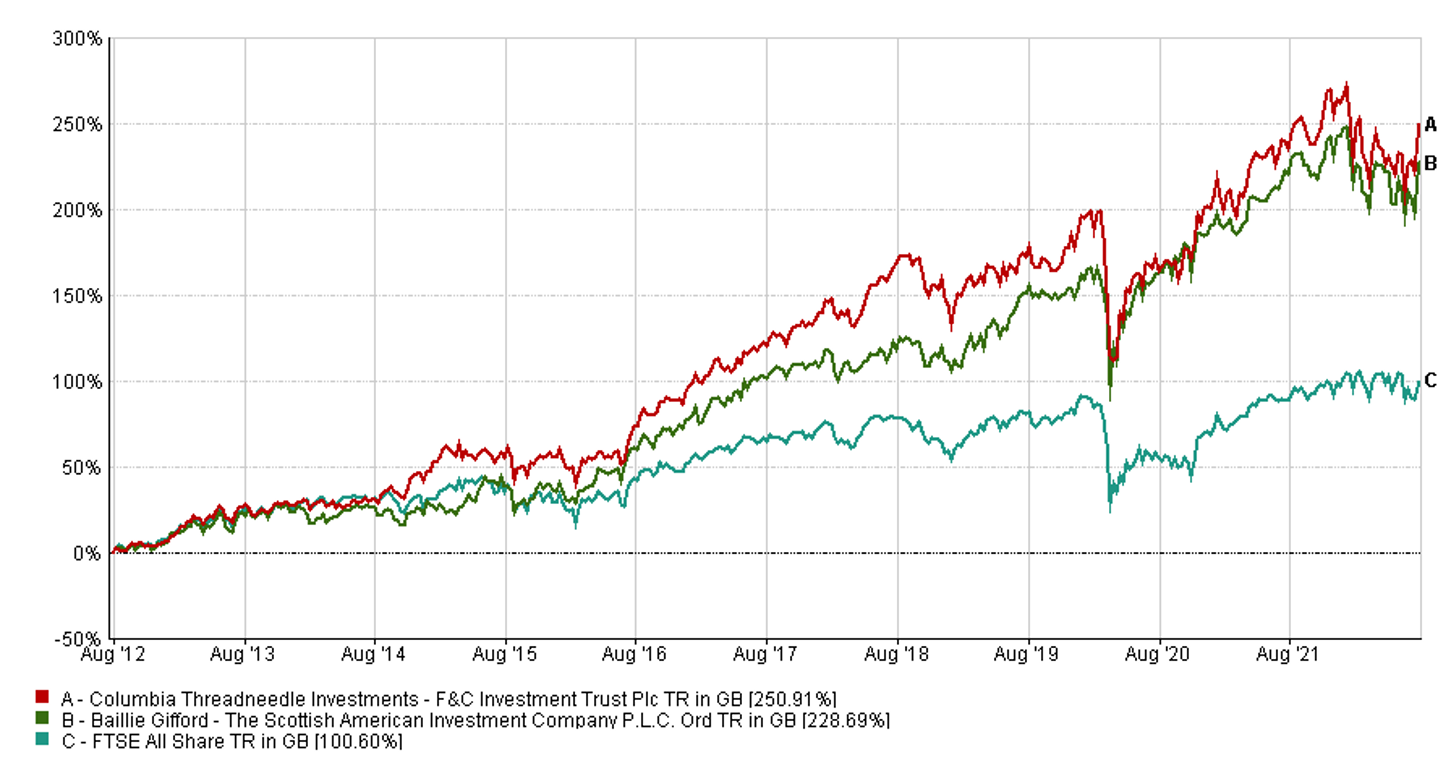

Two investment trusts vs index

“The chart shows two generalist, broad mandate investment trusts comparing their cumulative growth to the FTSE All Share – they have clearly trumped the index.

“In both cases, these funds that do not set out to beat the index do actually achieve that – perhaps one might conclude that is because these active fund managers are applying strategies that actually work to deliver better risk adjusted, management fee paid for, returns? The figures would support that premise.”

The latest AJ Bell Manager versus Machine report found that less than a third of active equity funds have beat their passive equivalents so far this year. That is down from 34% in 2021.

According to the report, only 12% of active funds have outperformed a passive alternative in the UK.

In the US, 40% of active funds outperformed, that is a marked improvement on just 19% last year.

Kingswood head of investment management Paul Surguy said: “The first half of 2022 was not enjoyable for most investors. Asset classes pretty much across the board, with the exception of gold and commodities fell in value.

“At times like these, investors will often look to the cost of their investments and question if their assets are worth what they are paying for.

“The first place that many will look is to active investment versus passive.”

Commodities and gold are only assets with positive returns

Surguy stressed that clear arguments can be made in favour of both investment styles.

He added: “The cost benefit of holding a passive investment does need to be balanced by the fact that one has market weighted exposure to all assets.

“For example, going into the financial crisis financials fell from 22.2% of the S&P to 11.9% in six months. An active investor would be able to have less financials, or even none.

“Of course, the opposite has been true in 2022 where energy and materials, sectors that have been in multi-year declines, making up a significantly smaller portion of the S&P than they have historically have shone. In the UK, holding a FTSE 100 tracker would have been positive for many investors.”

Informed Choice director of client education Martin Bamford believes that the active vs passive investment debate is more important than it should be.

He said: “The value of active versus passive fund management is often overstated, as the bulk in variance of investment returns come from asset allocation, not fund selection or market timing.

“The task of the financial planner should be to populate a chosen asset model as cost effectively as possible, and that’s likely to mean a large allocation to low-cost index tracker funds.

“However, there are other considerations at play too. Behaviour and emotion is critical to an investor actually enjoying the returns from a given asset over long periods of time.

“There’s no point in exposing an investor to extreme volatility, with the long-term goal of superior returns, if that strategy leads to sleepless nights and the investor abandoning ship at the wrong times.”

As a result, Bamford said that diversification, both at asset allocation and fund style levels, is what matters.

“ESG considerations are also crucial when building a modern portfolio, and passive funds are generally lousy at ESG,” he added.

‘Struggled, not failed altogether as we remember Bill Miller’s educational trumping of the index for 15 consecutive years whilst at Legg Mason’

Mr Doug Brodie should read ‘Winning the Loser’s Game’ by Charles Ellis, pages xi and xii of the forward.

I’m sure Charles wont mind me quoting a couple of paragraphs which can be viewed online here; https://is.gd/GXMABy

Simple performance reports fail to capture the impact of these numbers on investors. At the point of inception of the extraordinary streak, FUM amounted to $800m, exposing a relatively modest amount of investor assets to the begining of the excitment. Fifteen years later, assets ballooned to $19.7 billion, placing the maximum level of investors funds at the point of maximum bullishness. After three years of miserable performance and investor withdrawals, assets shrunk to a mere $3.4 billion.

Even though the simple time-weighted returns, as reported in the fund offering documents and in fund advertisments, tell a story of modest market-beating results, dollar-weighted returns tell a different story. Taking into account investor cashflows, dollar-weighted returns fall short of the S&P 500 result by a margin of 7.0% per annum. Over the 18 year period that includes the 15-year streak and the 3 year fall from grace, the once celebrated fund manager destroyed a staggering $3.6 billion of value for his investors.

Maybe Doug Brodie’s next example will be of a certain Mr Woodford’s exceptional returns…….