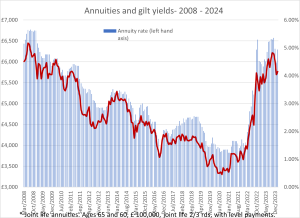

The great annuity revival started in the summer of 2020, when bond yields began to rise from the lowest point in recent history.

As the table below shows, the big leap in annuity rates came in 2022. In 2023, rates were stable, suggesting the peak has passed for the time being.

| Annuity income* | 15-year gilt yield | ||||

| Start | End | % change | |||

| 2023 | £ 5,993.88 | £ 5,986.32 | 0% | 3.96% | 4.04% |

| 2022 | £ 3,947.00 | £ 5,993.88 | 34% | 1.25% | 3.96% |

| 2021 | £ 3,821.00 | £ 3,947.00 | 3% | 0.54% | 1.25% |

| 2020 | £ 4,188.00 | £ 3,821.00 | -10% | 1.16% | 0.54% |

* Benchmark annuity – £100,000, ages 65 and 60, Joint life 2/3rds with level payments

The reason for the spike in annuity rates was that bond yields increased significantly. First, there were concerns about inflation, then the start of Ukraine conflict in February 2022, followed by the Mini-Budget in September 2022.

It seems bond yields have reached their peak for the time being and the trend is now downwards. Hopefully, this will be slow and gentle.

This means the outlook for annuities will be a slow easing of rates and slightly lower incomes, but they should still remain good value for money.

For old hands like me, it is easy to understand the relevance and importance of higher annuity rates, as we have advised clients through decades of change and turmoil in the pension market.

Back in 1990, when I first started collecting annuity data, the 15-year bond yield was nearly 12% and the benchmark annuity was over 15% (compared to about 4.5 % and 6.5% today).

In those days, it was compulsory to purchase an annuity. There was limited use of the open-market option and there were few enhanced annuities.

People cannot have their cake and eat it. That is, they cannot have both high income and lump sum death benefits

I still have clients who purchased annuities at these very high rates. Indeed, I recently received a phone call from one, now almost 100, to thank me for my advice, saying he had definitely won his bet with the actuaries and got more than his money’s worth from his annuities.

In the late 1990s, annuities became very unfashionable, not least because of the unfavourable coverage in the national press, with headlines such as: “Annuities are legalised theft.” (I was unfortunately quoted as saying, “Insurance companies are screwing their clients.”)

However, it was pension freedoms that knocked the final nail into the coffin. The new flexibilities and impression that drawdown was better than an annuity, coupled with very low annuity rates, reduced their appeal and demand drastically.

As I am constantly reminded, there is a generation of advisers who have little experience of annuities and have grown up with the impression it is better for clients to invest in Sipps and drawdown. To put it another way, maximising income from pension pots has been replaced by emphasising flexibility and the option to leave pots to beneficiaries.

Annuities give peace of mind and financial security, whereas during times of volatile markets, drawdown can be a rollercoaster

So, what words of wisdom do I have for those who have little experience of advising on annuities?

First, take the trouble to understand their advantages. It is simple to see annuities as a policy that guarantees income for life. A more sophisticated view is to think of them as providing the optimum distribution of income over the lifetime of the annuitant.

It helps to consider what would happen if there were no annuities. Anybody wanting to convert their pension pot into income would be faced with two important dilemmas: how much income to take and where to invest their money.

If they took too much income, they will run out of money and if they invested badly they would see the value of their pension fall. An annuity solves this dilemma by taking away both income and investment risk and ensuring the annuitant does not outlive their pension.

I recently received a phone call from one client, now almost 100, to thank me for my advice

Secondly, take a closer look at the numbers. It is easy to dismiss annuities as being poor value for money and, by inference, drawdown is better value. But a closer look at the numbers shows annuities are a hard act to beat if maximising income is the main objective.

Be honest with clients about the trade-offs between guaranteed income and flexibility. One of the main reasons people favour drawdown over annuities is the option to leave money to the family on death.

However, people cannot have their cake and eat it. That is, they cannot have both high income and lump sum death benefits. In practical terms, this means many people in drawdown will probably receive less income compared to annuities (unless there are significant higher returns from drawdown investments) because there is no mortality cross subsidy.

Finally, don’t forget the emotional and behavioural side of annuities. Annuities give peace of mind and financial security, whereas during times of volatile markets, drawdown can be a rollercoaster ride.

William Burrows is an adviser with Eadon & Co and runs the Annuity Project at www/williamburrows.com

Like all other articles about annuities (that I’ve read), this one talks about lifetime annuities vs. Income DrawDown as if there’s nothing in between which, of course, there is, albeit not without a measure of risk. The biggest drawback of a lifetime annuity is its total lack of flexibility. Once written, it can never be changed, no matter how much the circumstances of the annuitant may do so. Why does no one ever talk about temporary annuities?

Very well said re temporary annuities…

At around age 60, a 5n TA combined with a 5 year reducing term policy offered a good combination.

Asking anyone to decide at (around) 60 for the rest of their lives with their current circumstances is crazy… Guaranteed period, spouse, indexation, = fund cut by 50-60%.

Thus, the investment/mortality risk is removed by removing 50%+ of the initial fund… plenty of margin there then… Ouch!

When rates were 15%, granted, this WAS a deal to grab… but those times have past until probably 2032…

Do not forget that annuities work better the older you are – from 75 – and you may not have a spouse (say) to think about (too).

If you have a house, no mortgage, live off an income lifetime mortgage, pay this off and put some cash in your sky at age 75 when Equity Release will be high… + vest then. (Property value increasing at, average, 3% per year).

And… your own health may be impaired – 30% of all cancers appear in the 65-80 age group.

There is plenty of opportunity to beat Annuities in the short term bond markets, and provide AAA security with share short position arbitrage…

This more holistic than continually beating the same drum…

A friend of mine oversaw the ‘run off’ of Eq. Life… Quite a few policy holders were disappointed with NO peace of mind when they came to cash in!

It is a good point Fixed term annuities (or whatever they are named), saw a big uptick in business last year.

Best estimates put the fixed term annuity market at around a billon pounds last year.

And… the older you get the better the terms!

+ you know your (remaining) future better at, say, 70 than 55/60.